Cross-border banking is a service that allows individuals and businesses to use banking services regardless of where they are. A person can live in a country that is not his home country and still use banking services that overcome the disparity between the two currencies, the rules and regulations that govern banking in both countries, or even the operational procedures that apply to organisations involved in each transaction.

It can be as simple as automatic bill payment, but when it comes to paying a bill incurred in another country, different entities are involved on both sides of the border, different laws govern the process on both sides, and there is a currency difference. Cross-Border banking overcomes all of this to provide convenience to the end user in the same way that domestic banking does.

The scope of cross-border banking includes opening a bank account for any currency, making an international money transfer to and from any country, obtaining a loan in any country, or making an investment in any country or any currency. With the increasing globalisation and advancements in transportation and communication technology, the world is closer than ever before.

As a result, today’s consumers expect to transact seamlessly, no matter where they are in the world. Whether the transaction involves shopping, investing, making payments, or obtaining loans, consumers expect that banking services are delivered to them in a manner convenient to them so that they are able to make hassle-free transactions.

In recent years, India’s outbound travel has been increasing due to a growing middle class, increased disposable income and the world becoming closer due to the factors mentioned above. Today, people can travel to explore a different country as a tourist or experience life there. They can travel to run a business or in search of an employment opportunity. They can travel looking for investment opportunities or opportunities to expand existing businesses.

Irrespective of the reason though, with this increase in outbound travel, money movement in and out of the country has also increased, and this increase has resulted in a growing demand for cross-border banking to be made easier and faster, with consumer protection and compliance, in essence, to be made more convenient.

To fulfil this growing demand, fintech companies are leveraging technology and have filled the gaps left unattended by traditional cross-border banking infrastructure for decades. In the past, this was done through the use of networks and correspondent bank relationships, but today neobanks aim to make this process seamless, faster, and consumer-friendly leveraging technology to ultimately deliver on the demand for convenience.

How India Sent & Spent Internationally Before Neobanks

Before the emergence of neobanks in India, individuals primarily utilised cross-border banking services through banks themselves, who relied largely on traditional methods that are inconvenient. Even today they haven’t completely managed to transform themselves. There is a humongous scope for improvement, despite the transformation they have undergone so far.

The process often involves opening a foreign currency account, which could be time-consuming and involves high fees. People also used intermediaries such as money transfer companies to send and receive payments, this mode also carries its own drawbacks such as high costs and lack of reliability. Here are some of the channels used for international money transfers:

- External Rupee Accounts (NRE/NRO): These accounts are opened by Indian nationals living abroad to facilitate remittances from foreign countries to India. The NRE account is used to park foreign currency earnings, while the NRO account is used to park the earnings in Rupee.

- SWIFT: This is a messaging network used by banks to securely send and receive payments. This payment network allows individuals and businesses to take electronic or card payments even if the customer or vendor uses a different bank than the payee. The SWIFT messaging system is used by banks to make international money transfers and is the largest and most streamlined method for international payments and settlements today though technological advancements have enabled and empowered the rise of many challengers to dominance.

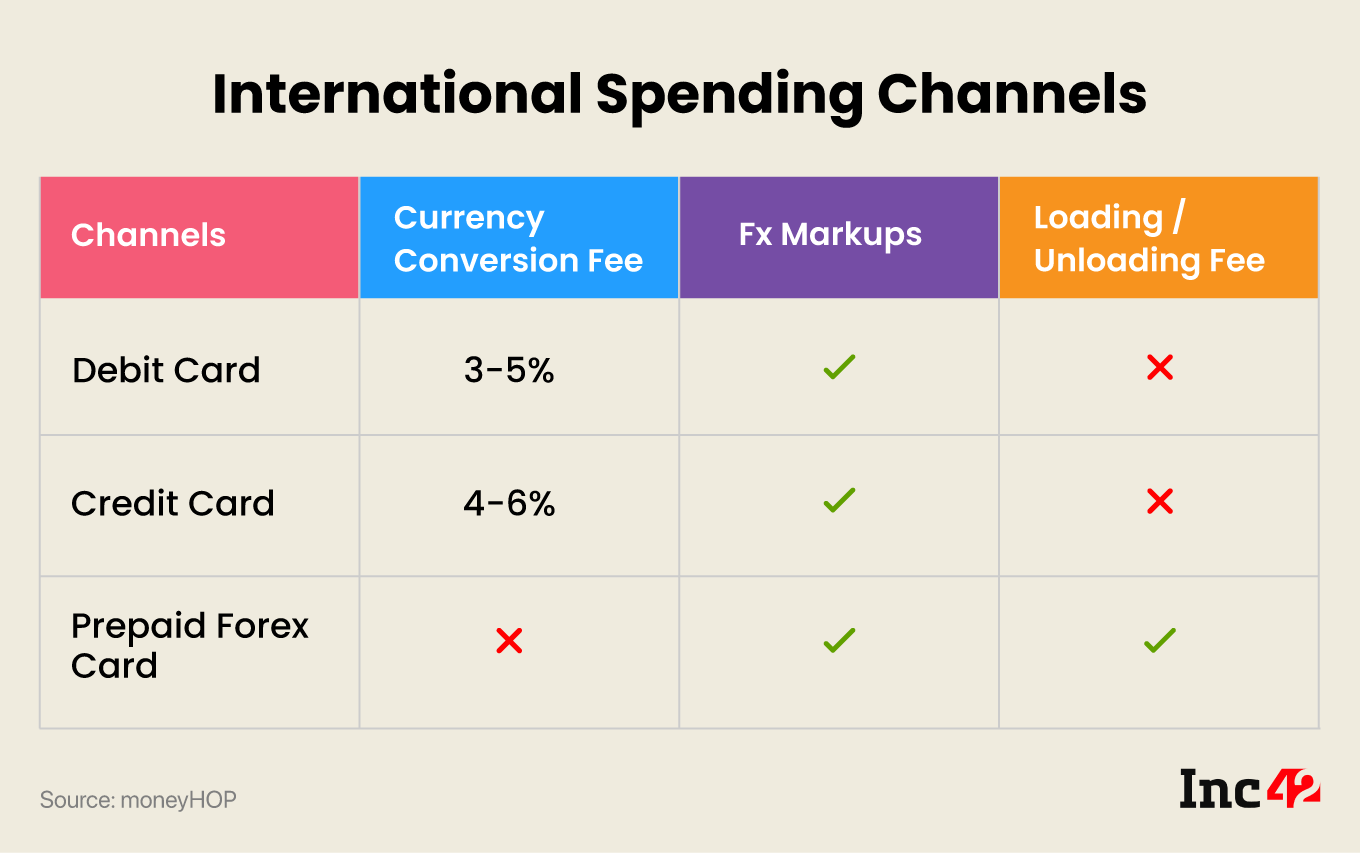

International Spending Channels

When travelling abroad, there are a few traditional ways to spend money, such as using credit cards, debit cards, or prepaid forex cards.

- Credit cards: Many credit cards allow for international transactions and can be used at merchants or ATMs worldwide. One of the major problems associated with credit cards is the high transaction fee that is charged with International usage. Some issuers also charge fees to convert the currency, which will also go from the cardholder’s pocket.

- Debit cards: Some debit cards also allow for international transactions and can be used at merchants or ATMs worldwide. One major issue with using debit cards is that some banks may block transactions made outside of the country as a security measure. This can cause inconvenience and make it difficult to access one’s own money when travelling. Additionally, the debit card could have additional fees when used abroad such as currency conversion fees, ATM withdrawal fees, and foreign transaction fees.

- Prepaid Forex cards: Prepaid forex cards are largely accepted and unlike debit/credit cards, no cross-currency conversion charges are levied. However, the process to get a forex card is cumbersome. Also when one gets back from their trip, transferring the remaining money back to the account can be a hassle.

How Neobanks Are Improving Cross-Border Banking

Neobanks are often seen as a more convenient alternative to traditional banks or money transfer companies. Here are some ways neobanks are leveraging the technology to solve the challenges existent in cross-border payments:

- Automation of processes: Neobanks have revolutionised the banking industry by bringing automation to various banking processes. The elimination of the need to physically visit a bank has been a game-changer for cross-border transactions. With the use of neobanking applications, customers can initiate their transactions in just a matter of minutes and track their status in real time, eliminating the need to wait for manual bank processing. This not only saves time but also provides convenience and accessibility to customers.

In addition, processes such as Know Your Customer (KYC) and Anti-Money Laundering (AML) checks have been automated to be more efficient and secure. Automated checks ensure a faster, more consistent, and more accurate screening process, reducing the risk of fraudulent activities. In fact the rise of neobanks has also brought about large-scale digital transformation to banks and banking services globally.

- More Transparency: Neobanks offer greater transparency in cross-border transactions compared to traditional banks. Customers can easily access real-time exchange rates and compare them across different providers. The transparency provided by neobanks empowers customers to make informed decisions, giving them greater control over their finances. Customers no longer have to rely on banks to determine the best exchange rates and charges, as they have access to all the information they need to make the best choice.

In traditional banking, small markups can often go unnoticed and end up costing customers a significant amount. With neobanks, customers have access to more information and are better equipped to make informed decisions, reducing the risk of overpaying on cross-border transactions.

- Travel Cards: Neobanks have introduced travel-friendly Debit+FX cards that offer several advantages over traditional prepaid forex cards. These cards typically offer more favourable exchange rates and lower fees compared to traditional banks, making them an attractive option for international travellers.

One of the reasons for this is that neobanks operate primarily online and have lower overhead costs than traditional banks. This allows them to pass on savings to customers in the form of better rates and lower fees on travel-friendly Debit+FX cards.

Moreover, many neobanks have developed user-friendly mobile apps that make it easy for customers to manage their forex card while travelling. With real-time updates, customers can easily track their spending and monitor their account balance, reducing the risk of overspending and ensuring they stay within budget while abroad.

- Neobanks’ APIs being used by businesses: APIs, or Application Programming Interfaces, have become widely used by payment system operators for a variety of functions in payment processing and value-added payment services. One of the main reasons for the popularity of APIs in international money transfers is that they address various challenges in payment processing.

By using APIs, payment processing can become faster, more accessible, and less expensive. For example, by using APIs, money transfers can be processed in real-time, allowing for faster delivery of funds to the recipient. Additionally, APIs can provide access to a wider network of financial institutions and payment systems, enabling customers to transfer money to more countries and to more recipients. Finally, APIs can help to reduce the cost of payment processing by automating many of the manual processes involved, making it possible for financial institutions to offer lower-cost money transfer services to their customers.

- Security in terms of Technology: Neobanks are considered more secure than legacy banks in terms of technology because they employ advanced technology and security measures. For example, they use cutting-edge encryption to secure customer data and transactions, making it harder for hackers to access sensitive information.

Additionally, neobanks use two-factor authentication, such as biometrics, to verify customer identity, making it more difficult for fraudsters to access accounts. They also employ real-time monitoring to detect and prevent fraud, as well as continuously updating their software and security systems to stay ahead of emerging threats.

Way Forward

Neobanks are creating a paradigm shift in the way consumers and businesses alike, think about cross-border transactions and how they process payments and access funds. They offer a plethora of services like instant currency exchange, rapid account opening, money transfers, loans, Debit+Forex cards, and access to a wide range of ATMs anywhere in the world.

But more than this, what sets neobanks apart are the innovative features, easy digital interface, and supportive customer service they provide. In conclusion, for consumers the real value of neobanks is convenience. From account opening to card blocking everything can be done on the phone itself. Time will tell whether neobanks will rule or traditional banks will equip themselves with current disruptions.